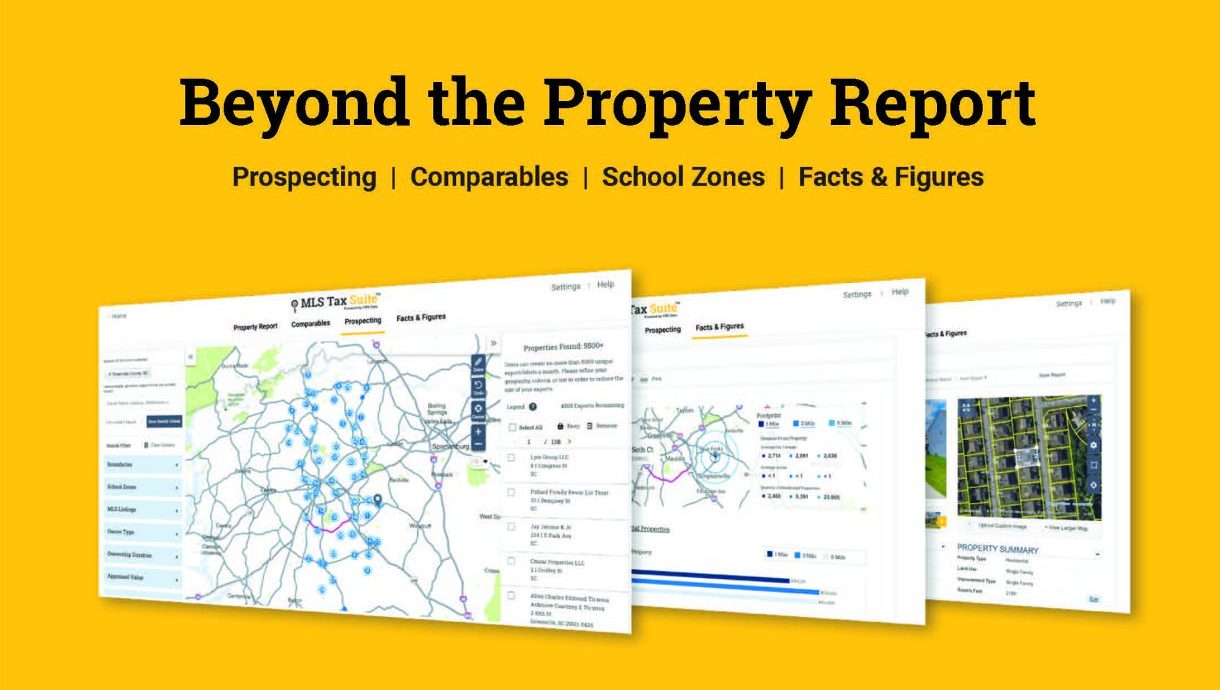

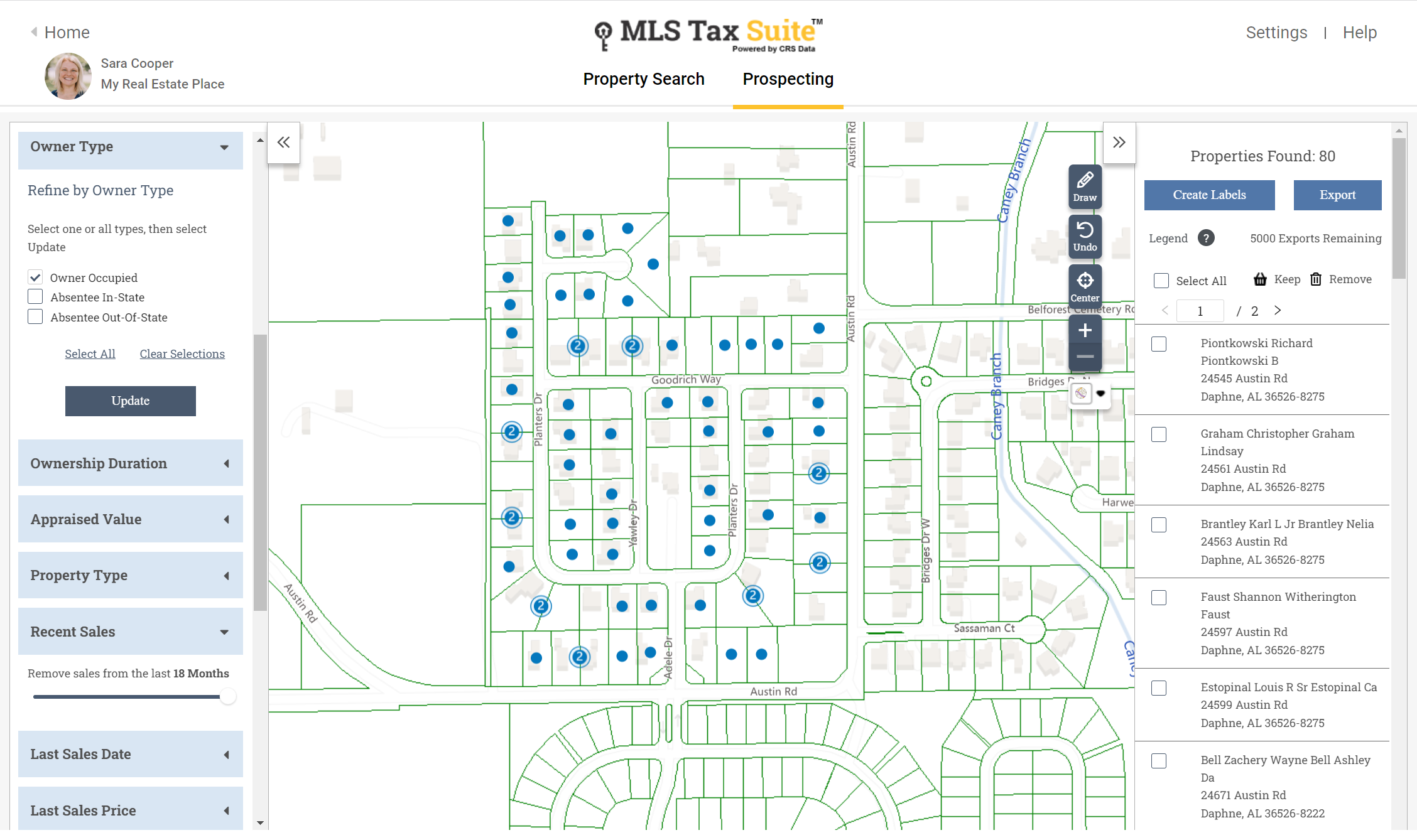

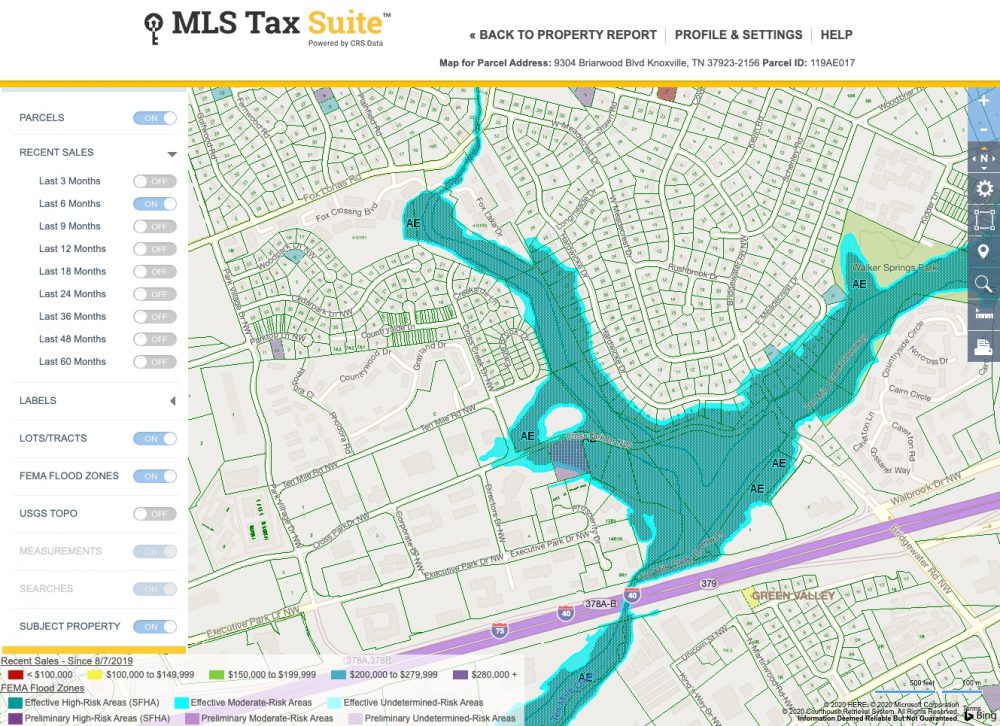

CRS Data Continues to Grow MLS Customer in 2026

CRS Data, a leading provider of real estate data and technology solutions, is proud to announce continued momentum across its MLS-facing products, MLS Tax Suite and ListingIntegrity. As MLSs navigate an increasingly competitive landscape and work to demonstrate their value to members and consumers alike, CRS Data’s solutions continue to act as an essential part […]